Since the start of the pandemic, self catering holidays have become exceedingly popular, and we see many common questions around how business owners can run a successful FHL, and how the tax works.

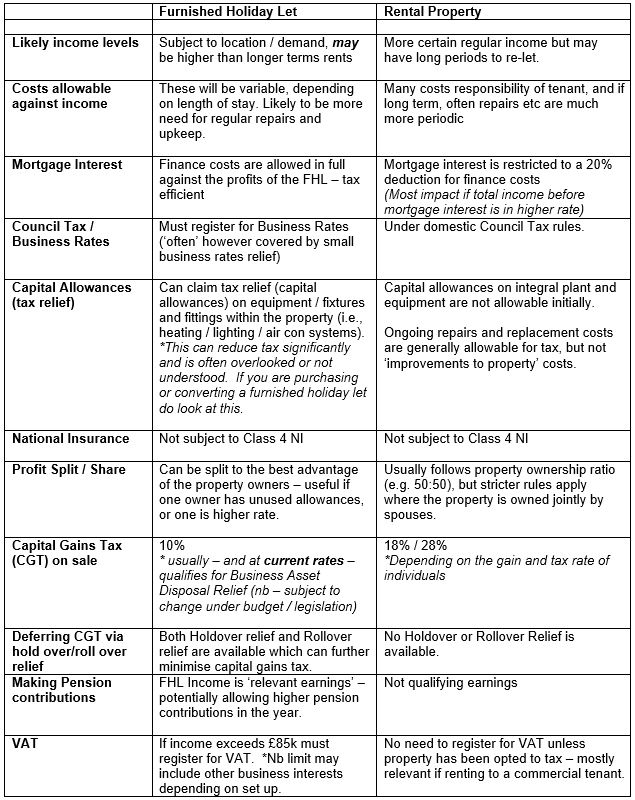

The table below therefore lists the main tax and national insurance implications and differences between FHLs and renting out properties for a longer term.*

There are of course many other issues and risks to consider if you are thinking about taking on any kind of investment property, and as always, there is no substitute for taking the right professional advice before you start. This guide concentrates on the main tax issues only, and does not take into account any planning or other building consent issues, and certainly does not act as a substitute for sound advice from a knowledgeable property managing agent.

What is a furnished holiday let in comparison to a ‘normal’ let property?

A Furnished Holiday Let is a property that meets several criteria based on occupancy – this criteria is assessed in each tax year, and broadly must meet the following:

• The property must be available to be let for 210 days in the year

• The property must ‘actually’ be let for at least half of this – 105 days per year

• The property must not have more than 155 days of letting that consist of stays exceeding 31 days (i.e. it is for short term lets)

• The property must be furnished (to allow people to occupy it)

If my property meets the criteria – how does the tax work? Click here to find out more.

{kind=link}

As you can see, there are a number of differences in tax depending on how a property is operated, there is no ‘one size fits all’ answer, but it is certainly useful to have an understanding of the above when making your decisions about how to ‘let out’ a property.

It is important to note that there are other ‘hybrid models’ that may mean income is treated as trading income, rather than furnished holiday let income. If you are thinking about offering ‘FHL’ type accommodation please speak to your advisor about the tax (and practical consequences).

Click here to read other Tourism Newsletter articles.