The Scheme

The Eat Out to Help Out scheme will be introduced to encourage people to return to eating out, thereby providing a boost in demand for cafes, restaurants and pubs. This will entitle every diner to a 50% discount of up to £10 per head on their meal, at any participating restaurant, café, pub or other eligible food service establishment. The discount can be used unlimited times and will be valid Monday to Wednesday on any eat-in meal (including on non-alcoholic drinks) for the entire month of August 2020 across the UK. Participating establishments will be fully reimbursed for the 50% discount and can register for the scheme now.

Are you eligible?

Eligible establishments are those in which food is sold for immediate on-premises consumption (any take away only establishments are not eligible for the scheme). This includes:

- Restaurants

- Cafés

- Public houses that serve food

- Hotel restaurants

- Restaurants and cafes within tourist attractions, holiday sites and leisure facilities

- Dining rooms within members’ clubs

- Workplace and school canteens

If you’ve recently submitted an application to the Local Authority to operate as a food business then provided you submitted your application to the relevant local authority on or before 7 July 2020, you will be eligible for the scheme.

How do I register?

You can register for the scheme now and registration will close on 31 August.

To register, you must have:

- your Government Gateway ID and password (if you do not have one, you can create one when you register)

- the name and address of each establishment to be registered, unless you are registering more than 25

- the UK bank account number and sort code for the business (only provide bank account details where a BACS payment can be accepted)

- the address on your bank account for the business (this is the address on your bank statements)

You may also need your:

- VAT registration number (if applicable)

- employer PAYE scheme reference number (if applicable)

- Corporation Tax or Self-Assessment unique taxpayer reference

If you are registering 25 establishments or less, you must provide the details of each.

If you’re registering more than 25 establishments that are part of the same business, you do not have to provide details for each one. You should provide a link to a website which contains details of each establishment participating in the scheme including the trading name and address. You may also need to provide a list to HMRC on request, with details of all participating establishments.

You can register now using the below link:

https://www.gov.uk/guidance/register-your-establishment-for-the-eat-out-to-help-out-scheme

What happens once I’m registered?

You’ll be registered instantly and will receive a registration reference number – you’ll need this when you claim the reimbursement.

You’ll be added to a list of registered establishments that will be available to the public. The list of registered establishments is not available yet. You can also download promotional materials to help you promote the scheme and let your customers know that you’re taking part.

If you want to be removed from the list of registered establishments, you should contact HMRC who will remove you manually. This is not immediate, so you must tell customers that you are no longer offering the discount.

You should wait until you’re registered before you offer discounts to your customers. You cannot offer discounts before 3 August.

What records do I need to keep?

For each day you’re using the scheme, you must keep the following records:

- Total number of people who have used the scheme in your establishment

- Total value of transactions under the scheme

- Total amount of discounts you’ve given

If you are using the scheme for more than one establishment, you must keep these records for each.

When can I make a claim?

- You cannot claim yet. The service you’ll use to claim reimbursements will be available on 7 August 2020 and the service will close on 30 September 2020.

- You must wait 7 days from registration to make your first claim. HMRC will pay eligible claims within 5 working days.

- You will be able to submit claims on a weekly basis.

- You’ll still need to pay VAT based on the full amount of your customers’ bills.

- Any money you receive through the scheme will be treated as taxable income.

What sales are eligible for the discount?

The discount can be applied to food and/or non-alcoholic drink purchased for immediate consumption on premises, up to a maximum discount of £10 per diner (inclusive of VAT). There is no minimum spend requirement.

What sales are NOT eligible for the discount?

The discount cannot be applied to the following items:

- Alcoholic drinks

- Tobacco products

- Food or drink that is to be consumed off premises

- Food or drink that is sold as part of a private party, event or function taking place within an eligible establishment

It should also be noted that any service charge applied is not eligible for the discount.

When should I offer the discount?

When you register for the scheme, it is expected that you will offer it during the whole of your opening hours on all the eligible days that you are open and on all qualifying sales of food or drink. You can only offer the discount on Mondays, Tuesdays and Wednesdays, when your business is open. If a customer is dining in and then takes away the remainder of their meal, the discount will still apply.

Can I use the scheme in conjuction with other offers?

You can use the scheme alongside other offers and discounts you are offering. However to calculate the value of the transaction and make a claim to HMRC, you must first apply any special offers, vouchers or discount schemes you might be promoting or accepting and deduct any service charge. You will only be reimbursed for the qualifying discounts you provide as part of the scheme.

What counts as a diner?

A diner is any person, adult or child, for whom food or drink is being purchased for consumption on premises. A diner does not need to be the paying customer. Where there is more than one diner on a single bill, the cap does not need to be calculated for each individual diner based on their specific orders. Instead, the discount that is applied to the overall bill should be capped at the number of diners multiplied by £10.

Working examples of the discount being applied

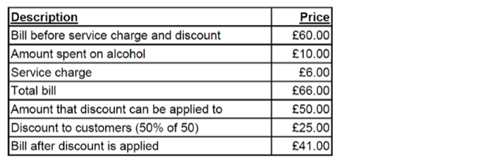

Example of applying the cap to a £60 bill:

A group of four diners (2 adults and 2 children) spend £60, including £10 on alcoholic beverages. There is a 10% service charge bringing the pre-discount bill to £66.

The total discount is £25, which is £6.25 per diner and is below the £10 per diner cap.

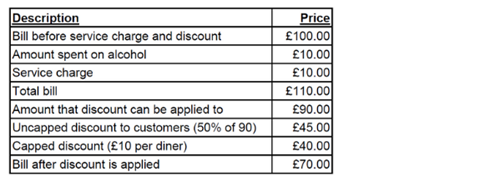

Example of applying the cap to a £100 bill:

A group of four diners (2 adults and 2 children) spend £100, including £10 on alcoholic beverages. There is a 10% service charge bringing the pre-discount bill to £110.

The uncapped discount is £45, which is £11.25 per diner and is above the £10 per diner cap. The discount is therefore capped at £40.

If you require any assistance with this scheme then please get in touch with your usual Dodd & Co contact.